Career Advice

Luxury Poverty: The New Definition of Success

Learn how luxury poverty reflects modern spending habits, shifting values, and the new definition of financial success.

Published on

December 3, 2025

Updated on

December 3, 2025

Luxury poverty describes a situation where people seem financially secure because they indulge in small luxuries, but behind the scenes, they struggle with bigger financial responsibilities, such as buying a home, saving for the future, or paying off debt. This concept is often linked to the younger generations, but it isn’t as simple as just overspending. Luxury poverty reflects a modern tension between enjoying life now and coping with economic pressures that make long-term stability feel out of reach.

Since moving to Spain almost ten years ago, I’ve had a front-row seat to two different versions of adulthood.

I see my childhood friends back at home buying houses, getting married, and saving for the future. Then there are my expat friends who haven’t made roots, but are rich in memories, travels, good food, and clothes we probably don’t need (but absolutely love).

That contrast got me thinking about a growing trend that captures this divide: luxury poverty.

To be clear, this isn’t about people experiencing genuine poverty. Instead, it’s about those posting beach vacations, dressed in the latest trends, smartphone in hand, while quietly stressing about rent, savings, or whether they’ll ever afford a home. (I’ll admit, I’ve been there.)

But the situation is more layered than simply “spending too much”. So, let’s unpack what’s really going on behind this new money mindset.

And if you want to find a job that can give you more financial stability, get started with our free AI Resume Builder to get a customized job application in minutes.

What Is Luxury Poverty?

Luxury poverty is when people look like they’re doing well financially because they indulge in small luxuries. However, behind the scenes, they’re struggling to afford the big things that some define as long-term stability, like owning a home, saving for retirement, or paying off student loans. This has become a growing trend for Gen Z.

We all know someone who drinks $6 lattes, with the latest iPhone, editing their vacation pics while their credit card balance quietly haunts them in the background (or maybe that’s you).

That’s luxury poverty.

Now, before we start painting the younger generation with the same brush, let me clear this up — not everyone fits this mold. In fact, there’s plenty of data showing that younger generations are taking their finances seriously.

A study published late last year by the Investment Company Institute found that Gen Z is actually outpacing previous generations when contributing to retirement accounts. So clearly, it’s not all avocado toast and impulse buys.

Intuit’s Beyond the Budget survey also found that 58% of 18- to 35-year-olds are intentionally weaving financial management into their overall wellness routines. More young people are recognizing that money stress impacts mental health, and they’re doing something about it.

Learn more about the realities surrounding the younger generation:

Spend Now, Worry Later: Everything’s Become So Expensive Anyway

Luxury poverty and the “spend now, worry later” mindset reflect a growing cultural trend, especially among younger generations. It’s about prioritizing living well now, even if it means stretching finances a little thin. It’s not always about being careless, but finding small doses of joy or control in an uncertain world.

Let’s take a look at what’s behind this attitude.

Living in the moment

The term “YOLO” might be past its sell-by date, but the concept is very much alive and kicking.

At 31, I’m at the age where earlier generations were getting married, buying homes, and starting families. But those traditional milestones? They just don’t hold the same weight anymore.

According to the State of the Consumer 2025 report, Gen Zers are less likely to define themselves by life stage achievements and more by personal experiences or passions. So, it makes sense that despite 43% of Gen Z admitting they’re not currently on track to save for retirement, spending still isn’t slowing down.

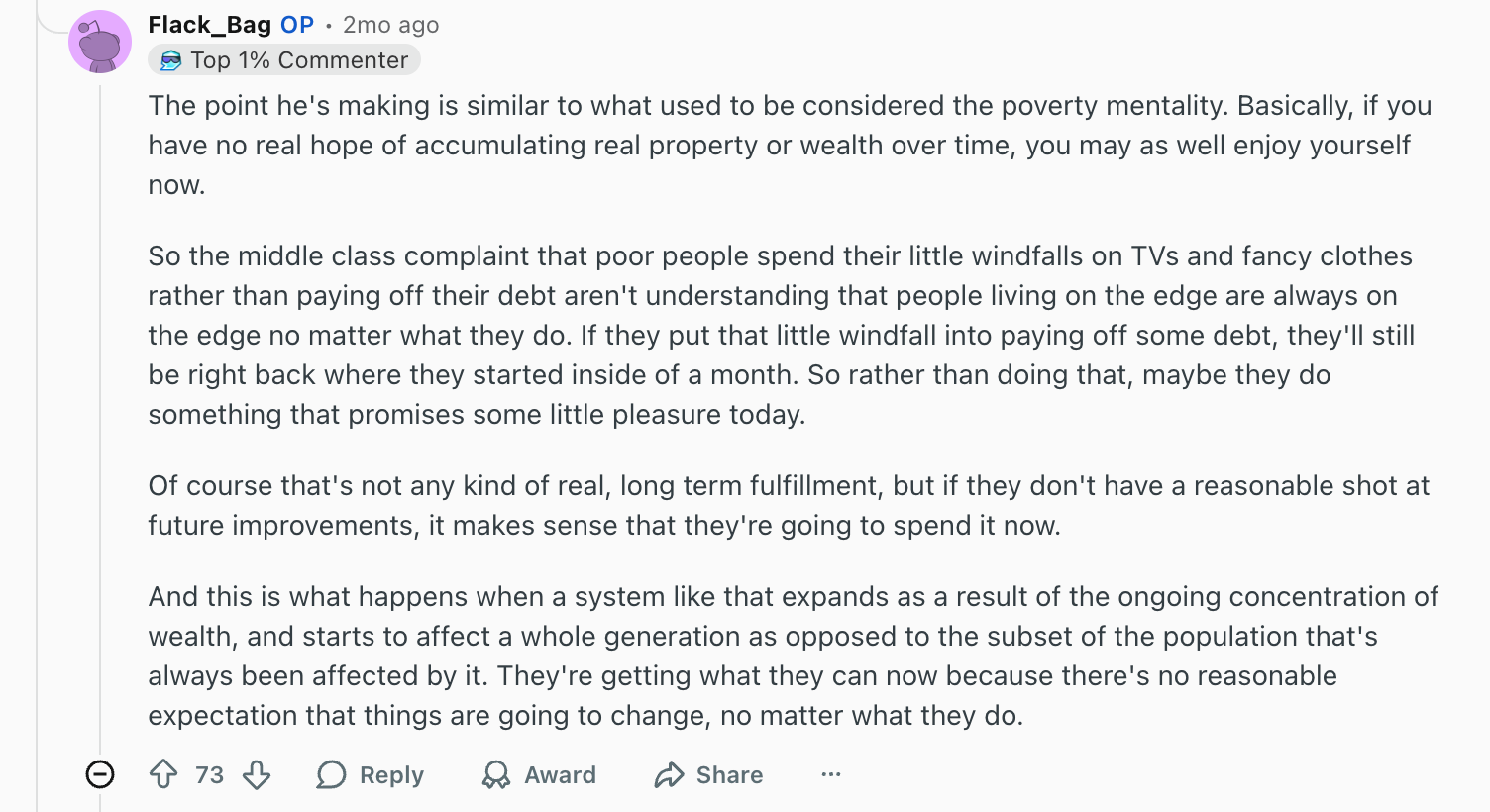

So why is this? I found this argument on Reddit that sums it up pretty well:

It’s not that we don’t want to save; it’s that it feels almost impossible or pointless in today’s economy.

Here are just a few disheartening facts that show why it’s become harder to save:

- In the past twenty years, home prices have outpaced paychecks by a wide margin. Over 90% of U.S. counties have seen rents and housing costs climb faster than typical incomes between 2000 and 2020.

- Grocery prices jumped 0.4% from July to August 2025 and were 2.7% higher than a year earlier. Overall, food costs in 2025 are expected to grow faster than usual, with total food prices projected to rise about 3%.

- Since 2000, hospital costs have surged more than 250%, about double the growth rate of overall medical expenses and roughly three times faster than general inflation.

- Average electricity prices jumped 7.4% in September this year, reaching a record 18.07 cents per kilowatt-hour — the largest increase since late 2023. Energy prices are also expected to continue upward into 2026, affecting transportation and commercial users.

When long-term goals like homeownership seem out of reach, buying small luxuries that spark joy feels like a rational emotional tradeoff. Psychologists call this “dopamine spending” — those little bursts of happiness that help people feel in control when everything else feels uncertain.

Shifting priorities

Most of us have faced this dilemma: the desire to save for the future and the urge to find comfort in the present. There’s a constant push and pull. One day focused on budgeting, the next convincing ourselves we deserve that meal out.

Gen Z embodies this tug-of-war. Their spending is growing twice as fast as previous generations did at the same age, and they’re on track to outspend baby boomers globally by 2029. Even though many aren’t earning big paychecks yet, they still make room for little luxuries.

These statistics from a Bank of America study reflect these spending habits:

- 57% of Gen Z buy themselves a small “treat” at least once a week.

- 59% say those treats often lead to overspending.

An overpriced coffee or a new skincare routine can easily turn from a quick pick-me-up into blowing the monthly budget. We’re also seeing a shift from saving for milestones (like a home or wedding) to prioritizing lifestyle and experiences. And all that student debt? That’s become normalized as just another joy of “adulting”.

Social media and the illusion of wealth

Then there’s the not-so-secret influencer in the room: social media.

It’s completely reshaped how people discover, evaluate, and buy products. I can’t count how many times I’ve given in to the social media hype and bought a trending beauty product (spoiler: most are disappointing).

For younger generations, these platforms are more than entertainment. They’re shopping destinations, consumer pressure, and social validation all rolled into one.

Here are a few stats to show the power of social media:

- Over a quarter of Gen Z use social platforms to find products.

- The influencer marketing industry is projected to hit $32.55 billion globally by 2025, and over 80% of marketers say it’s highly effective.

- 29% of consumers across the U.S., U.K., and Germany have bought a brand they discovered on social media.

Whether it’s a TikTok unboxing, another Labubu video, or a travel vlog, influencers make spending feel relatable, almost like a recommendation from a friend. The problem? It blurs the line between aspiration and pressure.

Social media has also given rise to what some call “aesthetic spending” — buying things not just for function, but to match an idealized version of yourself. And younger generations have fully embraced this, with 53% having used social “buy” buttons directly. It’s easy to see how curated luxury becomes the norm when every scroll shows someone living a perfectly filtered life.

Consumer Culture: Owning Less but Having More Stuff

We’re living in a paradox. People today own less in the traditional sense: fewer homes, fewer cars, fewer long-term assets.

Yet somehow, our lives are filled with more stuff than ever. Closets bursting with clothes, endless streaming subscriptions, drawers full of gadgets… It’s the modern version of abundance, minus the stability.

Essentials to excess

Let’s start with how “affordability” has flipped.

Those life-changing purchases, such as homes, education, and long-term investments, feel farther away than ever. And while the smaller luxuries haven’t necessarily gotten cheaper, they do feel more attainable. Yes, a new phone or a weekend trip still costs money, but they’re certainly more doable (and immediate) than saving for a house.

You can pick up a smartphone that fits in your pocket, but owning the roof over your head? That’s a completely different kind of math.

According to an Intuit survey, here’s what younger generations are claiming are the main culprits for financial stress:

- Increase in cost-of-living pressure (76%)

- Job instability (48%)

- Rising housing expenses (46%)

It’s not that people don’t want to save for the big things; it’s that costs just keep rising.

A GWI report found that only 6% of Gen Z plan to buy property anytime soon. Engagements are also down 25%, and plans to marry have dropped 16% since early 2024. And a Strat study revealed that 35% of non-homeowners have given up on saving for a home altogether.

So why do people keep spending instead of saving? Here’s an interesting argument:

It’s a pattern that actually started with my generation, the Millennials.

Many of us entered the workforce during financial instability and recession. We learned that job security could disappear overnight, so buying quickly took a backseat to renting. I don’t necessarily prefer it, but the financial landscape left little choice.

It doesn’t help that we’re constantly surrounded by influences (I’m looking at you, social media) that encourage us to spend on things we don’t really need, like designer clothes, the latest Apple phone, or beauty trends.

And while it feels easy to swipe for these small indulgences, saving or investing for the bigger things that actually matter often feels completely out of reach. It’s no big shock that so many of us end up juggling fleeting pleasures with financial stress.

Popular purchases

So, what exactly are younger generations spending their money on? Mostly tech, fashion, travel, and food — the cornerstones of modern comfort and identity.

A Mintel report found that:

- 70% of Gen Z spending goes toward clothing and footwear.

- Over half of U.S. Gen Z consumers spend on entertainment, such as video games, streaming subscriptions, and digital experiences.

- Around 38–46% regularly buy electronics like headphones or smartphones.

And according to the State of the Consumer 2025 report:

- 34% of Gen Z splurge on apparel.

- 29% spend heavily on beauty products (guilty).

With online platforms like Amazon Prime and Instacart, we’ve entered an age of instant gratification.

Gen Z, raised on fast internet and faster trends, expects shopping that’s efficient, flexible, and personalized. Why wait for the future when you can have a little piece of happiness arrive tomorrow (with free shipping)?

Advertisers have also played a major role in normalizing this mindset. We’re constantly told it’s okay to treat yourself with lifestyle upgrades: clothes, beauty, gadgets, meals out. After all, “you deserve it,” right?

This Redditor made a similar point:

But while those purchases deliver short-term satisfaction, they often come with long-term costs. The more we buy to feel “enough,” the further we drift from building actual financial security.

Want to earn more money to fund these purchases? Take a look:

Can Luxury Poverty Be Solved?

Short answer: Luxury poverty isn’t purely reckless; economic pressures like high housing costs and stagnant wages make long-term stability feel out of reach. Solutions involve personal action, such as budgeting, side hustles, and financial literacy. But it also comes down to broader economic changes. In general, ‘solving’ luxury poverty means redefining what “luxury” means, balancing joy today with financial security for tomorrow.

Is luxury poverty something we actually need to “fix”, or is it just a natural reaction to living in a time when the cost of living feels sky-high and long-term goals seem out of reach? This isn’t just about money — it’s about mindset, identity, and what we value in life.

Is luxury poverty even a problem?

It’s easy to look at “luxury poverty” and judge it as reckless spending, but maybe that’s oversimplifying things. Is this really a financial failure, or just a sign that younger generations are redefining what success and happiness look like?

Most people start their careers earning modestly, and yes, incomes often grow over time. So, the idea that you should enjoy your youth and not obsess over saving every penny does hold some weight. We’re only young once, after all.

On top of that, we also can’t ignore how different the landscape looks now. Traditional financial milestones, like homeownership, feel more out of reach. Many people have simply adapted by shifting their focus from owning things to experiencing life.

An NIQ report found that Gen Zers in the U.S. are less interested in settling down and more focused on:

- Earning well

- Building fulfilling careers

- Traveling, both globally and domestically

So, this isn’t laziness; it’s a cultural shift. Instead of chasing the same markers of success our parents did, we’re prioritizing flexibility, stability, and personal fulfillment. And interestingly, that approach can actually be healthier.

Despite different priorities, Bank of America found that 72% of Gen Z made moves over the last year to improve their financial health. That includes 51% who put money toward savings and 24% who worked on paying down debt. So while they might be buying flights and smartphones, they’re also quietly building better money habits.

Maybe luxury poverty isn’t so much a “problem” as it is a reflection of the times.

Possible ways forward

No one’s going to fix luxury poverty with a lecture about “just stop buying coffee.” The goal isn’t to guilt people out of enjoying life; it’s helping them build a lifestyle that feels good and makes financial sense.

Here’s what that could look like:

- Financial literacy without judgment. Learning about money doesn’t have to mean giving up every small joy. It’s about understanding where your money goes and making sure it aligns with what you actually value.

- Reframe luxury. True luxury could be financial stability, peace of mind, or even the freedom to take a vacation without guilt. Your budget, benefits, background, and beliefs all play into how you experience money.

- Align lifestyle with income. Focus on managing what you have realistically. That could mean cutting back on impulsive purchases, negotiating better pay, or simply getting clear about what’s worth your money.

Here’s what the younger generations are already doing to improve their finances:

- 41% of people say sticking to a budget has had the biggest positive impact on their money relationship (Intuit).

- When feeling financial stress, 90% of Gen Z say they take action, such as creating a budget (64%) or paying bills ahead of time (46%) (Bank of America).

- Side hustles are also gaining traction, with 41% of Gen Z and Millennials saying extra income streams have significantly improved their financial wellness (Intuit).

And if career growth is part of the plan (which it should be), updating your resume can help position you for that next big leap toward higher earnings.

Ultimately, solving luxury poverty is about redefining what luxury means to you. For some, it might be a new outfit; for others, it’s living debt-free or finally taking that dream trip without relying on credit.

But of course, we can’t ignore economic factors. High housing costs, rising living expenses, and stagnant wages make long-term financial security feel out of reach for many young people. Addressing luxury poverty involves both personal choices and an economy that makes stability achievable.

Final Thoughts

Luxury poverty is a modern contradiction that captures the complexity of finances and identity. It’s a reflection of how people are trying to find balance between survival, self-expression, and satisfaction in a world where traditional milestones like buying your own home feel impossible.

Younger generations are dealing with a very different economy than the one their parents grew up in. With homeownership and long-term security being significantly harder to reach, the focus has shifted toward small comforts and experiences that make daily life feel more meaningful.

But the concept also challenges us to ask what “wealth” and “success” really mean. Is it the number in your bank account, or the way you live your days? Maybe the real lesson is about intentionality: spending consciously, aligning choices with values, and finding satisfaction in what you already have.

FAQ

How can young people create financial stability?

Creating financial stability in your 20s or early 30s can feel like a losing battle, especially with rising rent and student debt. But stability isn’t about perfection. It’s possible to build habits and systems that protect your future while still enjoying life.

Here are some practical steps:

- Budget intentionally, but don’t deprive yourself. Track your income and expenses, but allow room for small joys. Even $20 a week for a treat is fine if you cover your essentials.

- Automate savings. Set up automatic transfers to a savings or investment account. You’re less tempted to spend what you don’t see.

- Invest early, even in small amounts. Compound interest is powerful. Even $50 a month in a retirement or investment account grows faster than you think.

- Diversify income streams. Side hustles, freelance work, or improving skills can help you deal with unexpected financial shocks.

- Build an emergency fund. Aim for at least 3–6 months of living expenses. Knowing you have a safety net reduces stress and prevents bad financial decisions under pressure.

How can you find a high-paying job?

Getting a high-paying job is about strategy, skill-building, and smart networking. Here’s how to approach it:

- Invest in your skills. Certain industries, such as tech, finance, healthcare, and business, tend to offer higher salaries. Upskilling through certifications, online courses, or advanced degrees can help you get there.

- Create a memorable resume. Tailor each job application to show how your achievements solve specific problems. Tools like Rezi can help you build a strong first impression.

- Network strategically. Connect with people in your target field, attend industry events, and engage online to open doors.

- Consider career mobility. Sometimes, switching companies or even industries is the fastest way to increase earning potential, especially early in your career.

Check out the highest-paying jobs and how to land them: Highest Paying Jobs in the US

Lauren Bedford is a seasoned writer with a track record of helping thousands of readers find practical solutions over the past five years. She's tackled a range of topics, always striving to simplify complex jargon. At Rezi, Lauren crafts genuine and actionable content that guides readers in creating standout resumes to land their dream jobs.

.webp)